![[Vantage Point] The uncomfortable math behind Jollibee’s MSCI demotion](https://i0.wp.com/www.rappler.com/tachyon/2026/05/MSCI-JOBI.jpg?ssl=1 "[Vantage Point] The uncomfortable math behind Jollibee’s MSCI demotion")

Jollibee’s downgrade from the MSCI Philippines Customary Index into the small-cap tier is extra a warning sign than a technical market occasion. It reduces the inventory’s visibility amongst world institutional traders and triggers portfolio allocations. Beneath the enduring model and aggressive worldwide growth lies a extra difficult monetary actuality: rising debt prices, tightening liquidity, mounting lease obligations, and a enterprise mannequin more and more depending on steady growth to maintain progress momentum.

This forensic evaluation reveals how this beloved Philippine client empire has advanced from a simple fast-food success story right into a extremely leveraged world roll-up now working below far stricter monetary and market scrutiny.

The relegation of Jollibee Meals Company from the MSCI Philippines Customary Index to small-cap isn’t just an embarrassing portfolio adjustment. It’s a forensic occasion.

Markets don’t demote companies primarily based on nostalgia, model affection, or nationwide symbolism. They demote them with liquidity, valuation dynamics, balance-sheet flexibility, and institutional confidence — all slowly turning off the boil.

And beneath Jollibee’s completely satisfied face and nonstop worldwide progress narrative, the monetary statements have now uncovered an organization within the throes of a way more ominous stage of company evolution.

With a view to really admire why that is vital, it’s good to get a deal with on what MSCI really is. Morgan Stanley Capital Worldwide, or MSCI, began within the late Sixties as a worldwide inventory market indexing and analytics company as a spot to assist institutional traders measure and evaluate markets worldwide.

Over time, MSCI turned one of the vital highly effective gatekeepers of world capital. At this time, trillions of {dollars} which are managed by pension funds, sovereign wealth funds, insurance coverage corporations, and exchange-traded funds check with MSCI indices to assist decide how cash ought to move.

In plain English, MSCI serves as a worldwide scorecard for publicly listed corporations. Big worldwide funding funds usually purchase or maintain the fairness of an organization that will get listed in the primary MCSI index.

There are a two fundamental nation indices within the MSCI. There’s an MSCI Philippines Customary Index and an MSCI Philippines Common Index. It’s vital to tell apart the 2 as a result of they serve totally different functions in world investing.

The Customary Index is MSCI’s main benchmark for Philippine large- and mid-cap corporations — successfully the nation’s institutional “fundamental stage” adopted by many world emerging-market funds, pension managers, and passive funding autos.

Inclusion indicators {that a} inventory possesses enough market capitalization, liquidity, and institutional relevance to warrant significant world investor publicity. Removing from that benchmark, subsequently, is just not merely beauty. It could set off computerized portfolio outflows and cut back the inventory’s visibility amongst overseas institutional traders.

The Common Index, against this, is a broader strategy-based spinoff index that comes with further portfolio and ESG-style overlays. Whereas helpful for specialised funds, it doesn’t carry the identical signaling energy because the Customary Index itself.

This distinction issues in Jollibee’s case as a result of its downgrade was tied to the primary MSCI Philippines Customary Index — the benchmark world traders carefully watch when assessing which Philippine corporations stay a part of the nation’s core institutional fairness story.

What it means

When an organization is downgraded right into a smaller class, these funds mechanically reduce publicity or exit altogether. For this reason Jollibee’s downgrade issues. Whereas it doesn’t imply the corporate is collapsing, uncertainty rises amongst world traders about Jollibee’s continued inclusion within the nation’s premier institutional-grade shares.

The reason being defined within the firm’s financials. Jollibee is just not financially distressed. It nonetheless recorded near P305 billion in revenues for 2025, in contrast with about P270 billion the prior 12 months. Internet earnings attributable to shareholders elevated a bit to round P10.9 billion. Thousands and thousands of Filipinos nonetheless patronize Jollibee shops, and the model stays one of many strongest client franchises within the nation. Deeply understanding Jollibee’s financials isn’t nearly revenues, however concerning the high quality of progress, and the way a lot monetary pressure is required to maintain it.

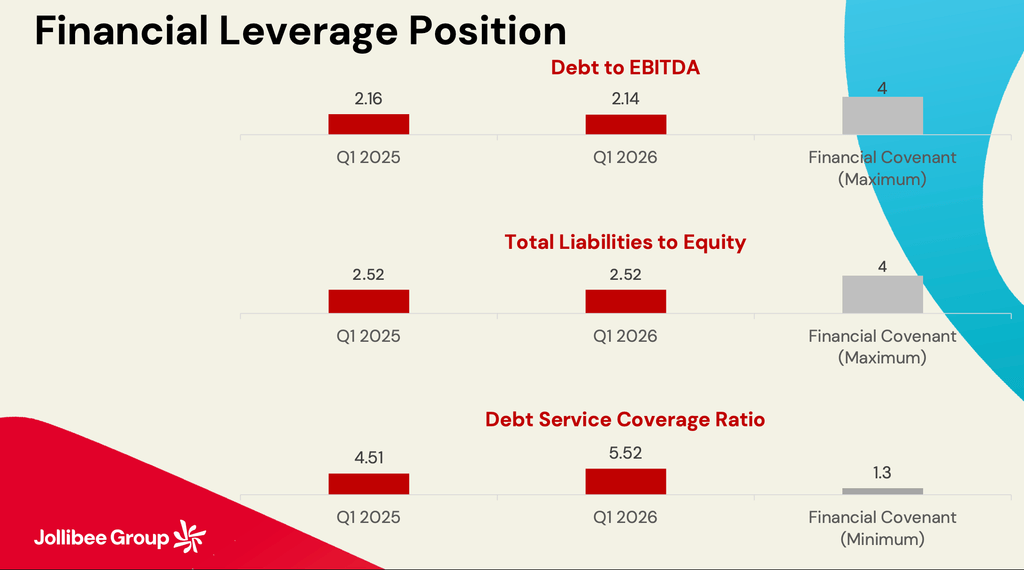

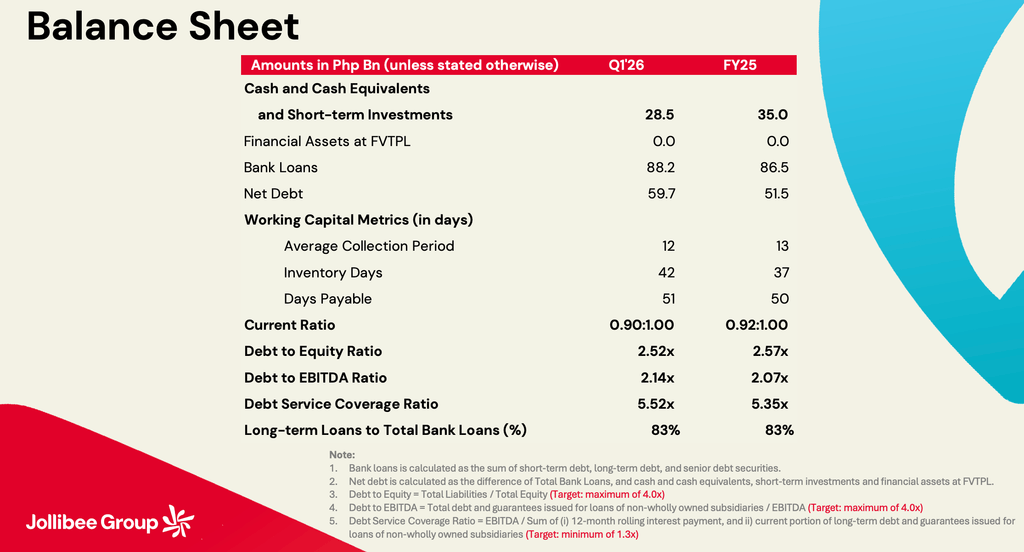

That is the place the stress turns into seen. Curiosity expense surged to roughly P7.6 billion from P5.8 billion in only one 12 months, rising a lot sooner than precise earnings. That issues as a result of rising finance prices quietly cut back the financial effectivity of growth. An organization can proceed opening shops and reporting larger revenues, even because it turns into financially tighter beneath.

Jollibee money owed outstrip belongings

Liquidity metrics reveal the identical sample. Present liabilities now exceed present belongings, pushing Jollibee’s present ratio beneath 1.0. In different phrases, short-term obligations are actually bigger than available short-term assets. This doesn’t imply insolvency is imminent. Jollibee nonetheless possesses sturdy banking relationships, monumental scale, and wholesome working money move. However it does imply the enterprise more and more relies on uninterrupted money era and steady refinancing situation.

The Jollibee Group is now a worldwide enterprise that could be a far cry from the normal firm many traders nonetheless image. For many years, Jollibee was considered one of many cleanest tales in Philippine capitalism: a homegrown fast-food chain beating world juggernauts by way of a mix of cultural acumen and self-discipline in operations.

At this time, the agency has grow to be a multinational acquisition middle depending on its debt markets, leases, and perpetual growth to maintain rising. That distinction fully adjustments its monetary danger profile.

Working money move was sturdy at roughly P36.7 billion. Capital outlays, nonetheless, exceeded a P15 billion price range, whereas leases have been consuming up practically P12 billion. Curiosity funds, dividends, refinancing obligations, and acquisition-related prices lowered liquidity much more. That is most likely what most retail traders overlook: being worthwhile on paper is just not the identical as producing out there money.

Too many cooks spoil the broth

An organization might report billions in earnings, whereas concurrently working below rising monetary stress as a result of too many events are competing for a similar money move stream. In Jollibee’s case, collectors require debt servicing, landlords demand lease funds, shareholders anticipate dividends, and world growth requires recent funding capital.

The rise of goodwill and intangible belongings should even be carefully thought of. Years of acquisitions pushed goodwill and emblems towards ranges approaching the dimensions of shareholders’ fairness itself.

Goodwill, in fact, is de facto an accounting assertion of optimism — the value administration pays as a premium for the excessive expectations of the enterprise, pushed by the assumption that any acquired enterprise will convey sturdy future earnings and long-lasting worth,

So long as these acquisitions maintain doing nicely, the technique pays off. However the bigger the goodwill turns into, in relation to fairness, the extra susceptible the stability sheet is, if progress slows or overseas operations fall brief.

That is exactly why the MSCI downgrade shouldn’t be handled as a one-time technical repair. It formalized what refined traders have been already beginning to see beneath the floor: Jollibee’s monetary standing has moved right into a harder interval through which progress alone is now not enough.

Traders need stronger free money move, higher liquidity, and extra stability within the stability sheet. Capital markets operate with arithmetic, not love. Traders care extra about exhausting numbers than model loyalty. That very same math is now questioning whether or not Jollibee’s worldwide empire can continue to grow with out increasing the monetary structure that underpins it. – Rappler.com

![[Vantage Point] Why Jollibee should stop thinking like a restaurant and start thinking like McDonald’s](https://www.rappler.com/tachyon/2026/01/JOLLIBEE-v-MCDO-1.jpg?fit=449%2C449)

![[Vantage Point] San Miguel’s profit surge — and the market’s skepticism](https://www.rappler.com/tachyon/2026/02/SMC-PROFIT-SURGE-FEB-24-2026.jpg?fit=449%2C449)

Click on right here for extra Vantage Level articles.