")

Miljan Živković/iStock through Getty Pictures

Healthpeak (DOC) is being valued as a combination between medical workplaces and labs. By property worth, nonetheless, it’s totally 25% senior housing. Senior housing values have dramatically expanded in current durations, but this worth has not proven up in DOC’s inventory worth. In response, DOC is spinning off its senior housing into Janus Dwelling (JAN) which, upon its IPO, ought to drive the market to instantly worth its senior housing property.

I consider the IPO will reveal the true worth of DOC’s senior housing as $4.25B relatively than the $3B at which they’re listed in its books. Over time, DOC can monetize its shares of Janus for a big supply of low-cost capital, which they will use to bolster their MOB and lab enterprise.

Allow us to start with a have a look at valuation after which dig into the upcoming IPO.

Valuation by property sector

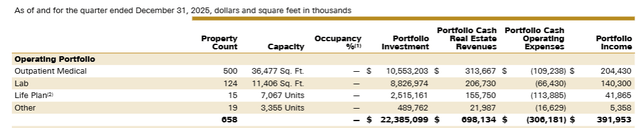

Utilizing price foundation, DOC has $10.5B in MOBs, $8.8B in labs and round $3B in senior housing.

Supplemental

Every of those sectors trades at considerably totally different valuations.

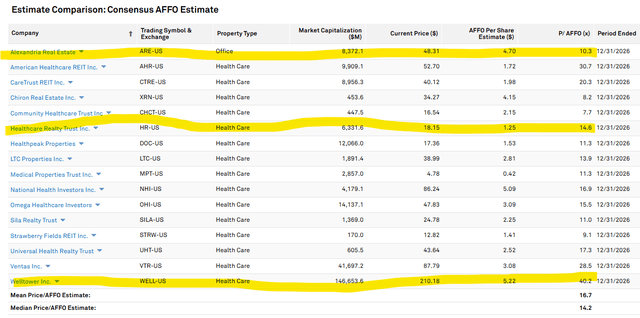

Labs are troubled presently with oversupply and commerce on the lowest a number of. Alexandria (ARE) is an almost pure-play lab REIT so it serves as a great approximation of the market a number of on labs.

Healthcare Realty (HR) is the closest to a pure-play MOB REIT, and Welltower (WELL) whereas not pure senior housing, trades at its excessive a number of nearly solely on its senior housing prospects.

S&P World Market Intelligence

As seen above these lab, MOB and SH comps commerce at 10.3X, 14.6X and 40.2X AFFO, respectively.

Healthpeak trades at 11.3X AFFO, proper between lab and MOB multiples. On an AFFO a number of foundation it might appear DOC shouldn’t be getting any credit score for its SH.

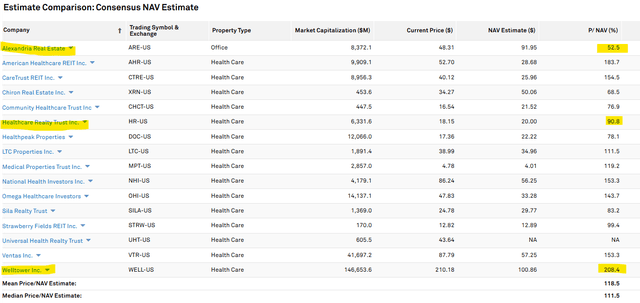

Internet asset worth tells an identical valuation story.

Labs commerce deeply discounted to NAV with Alexandria at 52.5%. Medical workplace, as measured by HR trades at 90.8% of NAV and senior housing proxy Welltower trades at 208% of NAV.

S&P World Market Ingelligence

As soon as once more, Healthpeak trades proper between labs and MOBs. DOC’s worth to NAV is 78.1%.

On each valuation metrics, DOC is clearly not getting credit score for its massive and robust senior housing portfolio.

Senior housing portfolio value about $4.25 billion

The capital invested figures offered earlier don’t correctly present the ratios of present day worth. Labs have misplaced worth, MOBs have roughly held worth, and senior housing has considerably elevated in worth.

That roughly $3B DOC invested in senior housing is value nearer to $4.25B at this time.

Particularly, DOC’s SH portfolio consists of 10,422 models throughout 34 communities with professional forma income of $771.2 million.

Prospectus

These communities are principally entry price based mostly the place residents pay a big (~$150,000) price up entrance to reside in the neighborhood after which transfer up the acuity chain as they age. DOC collects continued lease and medical revenues along with the upfront entry price.

As part of DOC’s bigger portfolio, the SH revenues have been neglected. As a standalone IPO, nonetheless, they fetch a a lot larger a number of. They’re focusing on an IPO worth for Janus Dwelling (JAN) of $18-$20.

We see this worth as extraordinarily believable because the providing is already effectively subscribed.

Per a Reuters report: “buyers CenterSquare Funding Administration, DWS Group, MFS Funding Administration, and PGIM have indicated curiosity in shopping for up to $300 million value of Janus shares from the providing”

These buyers alone account for almost half of the IPO which is meant to lift $635.5 million in web proceeds or a bit extra if the greenshoe is exercised.

As such, we will likely be utilizing the midpoint ($19 per share) as the premise of our calculations on the valuation of Janus.

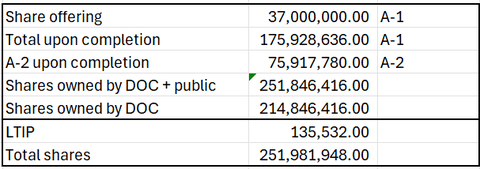

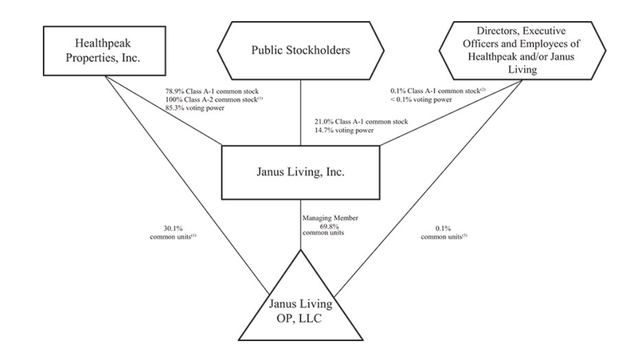

37 million A-1 shares are to be supplied within the IPO (plus a greenshoe).

2nd Market Capital

Healthpeak may even personal 78.9% of the Class A-1 shares and 100% of the 75.9 million A-2 shares. There are slight variations in voting energy between the shares, however for valuation functions, it’s the complete mixed variety of shares that we are going to be taking a look at.

DOC

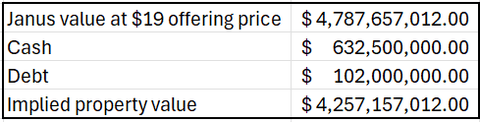

All-in there are to be a complete of 251.9 million shares of JAN. Utilizing the midpoint providing worth of $19 that’s $4.787 billion.

2nd Market Capital

Netting out money of $632.5 million raised within the IPO and including again $102 million of property degree debt, this means the senior housing property are valued at $4.257 billion.

Now allow us to study this valuation in relation to the contributed senior housing property.

They’ve the next monetary metrics:

- Professional forma estimated NOI of $199.6 million

- AFFO of $170 million

- Recurring capex of 29.9 million

- AFFO inclusive of capex of $140 million

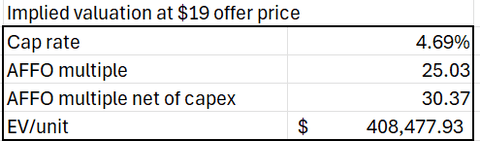

These metrics spot the IPO pricing on the following valuation ranges.

2nd Market Capital

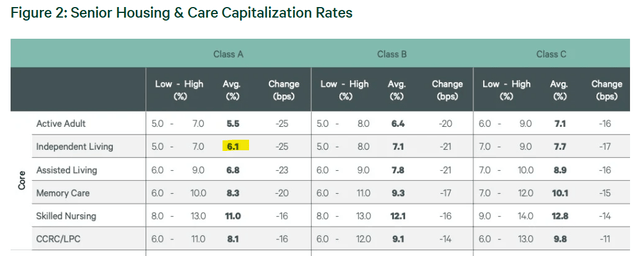

The cap price appears barely on the low aspect. CBRE figures spot the typical cap price for sophistication A senior housing at 6.1%.

CBRE

This report was from December of 2025 and senior housing cap charges have been trending downward. I believe they’re now within the 5s, however 4.69% for the DOC portfolio would point out its properties are of considerably larger high quality.

Implied enterprise worth per unit can be considerably above current comps.

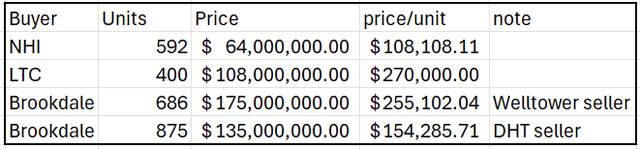

Senior housing acquisitions by Nationwide Well being (NHI), LTC Properties (LTC) and Brookdale Senior Dwelling (BKD) have been at worth/unit starting from $108K to $270K.

2nd Market Capital

Thus, the $408K implied enterprise worth per unit is effectively above common.

Variations can exist on account of kind of neighborhood. DOC’s entrance price life plan communities are notably prime quality which exhibits up within the profitability metrics.

AFFO per unit is kind of excessive, leading to a standard trying AFFO a number of regardless of the excessive price ticket per unit. JAN on the midpoint of the IPO vary trades at 25X professional forma AFFO or 30X strict AFFO.

That’s fairly a bit cheaper than Welltower’s 40X a number of. Nevertheless, as beforehand mentioned, I do consider Welltower is considerably overvalued. 30X, for my part, is way nearer to a correct senior housing a number of.

General, I discover the Janus IPO worth vary to be barely bold, however given how effectively subscribed the providing already is, I feel will probably be spot on.

Efficiently IPOing at this worth could be an enormous win for DOC.

DOC is presently valued as if it have been only a MOB/lab REIT. The market will instantly be pressured to acknowledge its $4.25B of senior housing, for my part.

Going ahead

Janus is poised to hit the bottom operating. They have already got acquisitions lined as much as instantly put the IPO proceeds to work.

DOC

As Janus grows, the worth will accrete to DOC because the shares will likely be held on its stability sheet for not less than a yr on account of lock-up.

Threat issue – AFFO accounting awkwardness

When REITs maintain shares of one other firm, the accounting will get slightly wonky.

With the senior housing property instantly owned by DOC, all of the AFFO produced by the properties confirmed up in DOC’s AFFO.

Because the properties are totally spun out into Janus, the property degree AFFO will not present up on DOC’s AFFO line. Whereas DOC will nonetheless owns them on account of its possession of Janus shares, earnings of Janus don’t stream via to DOC earnings.

To my data, there are 2 essential methods held shares will have an effect on DOC earnings:

- DOC can elect to earn modifications within the worth of the inventory. If Janus inventory goes up by $1 per share in 1 / 4, DOC can document earnings equal to ($1 * shares held). Related destructive earnings could be recorded if Janus inventory drops in 1 / 4.

- Dividends from Janus will be collected as DOC earnings.

Thus, DOC’s earnings are prone to be adversely impacted within the close to time period. Until JAN adopts a really aggressive dividend coverage, which I feel is unlikely, recorded earnings from JAN shares will likely be lower than the AFFO generated by the property.

This doesn’t matter in precise worth. DOC nonetheless owns the property via proudly owning JAN. It might probably, nonetheless, considerably affect the market worth of DOC relying on how effectively it’s communicated and the way prepared the market is to dig via the numbers.

The underside line

DOC is about to get credit score for substantial senior housing worth that was beforehand ignored. Whereas there will likely be unpredictable reception because the mud settles, I feel will probably be a transparent win by unlocking the worth in the long run.