![[Vantage Point] GSIS wagers on Citicore’s capital allocation](https://i0.wp.com/www.rappler.com/tachyon/2026/07/GSIS-CITICORE.jpg?ssl=1 "[Vantage Point] GSIS wagers on Citicore’s capital allocation")

Behind each profitable infrastructure firm lies one defining take a look at: can administration persistently flip billions of pesos of capital into sturdy shareholder returns? That query is on the coronary heart of the GSIS’ funding in Citicore.

The simplest technique to misunderstand Citicore Renewable Vitality Corp. is to guage it like an influence firm. It’s not, at the very least not but.

Immediately, Citicore is healthier understood as a capital allocation enterprise, deploying billions of pesos to assemble an vitality platform whose actual worth will emerge solely years from now.

That distinction explains why the acquisition by the Authorities Service Insurance coverage System (GSIS) of a 7.5% stake deserves neither automated applause nor unwarranted skepticism. GSIS shouldn’t be merely shopping for photo voltaic farms. It’s investing within the means of Citicore’s administration’s to remodel huge capital spending into future money flows that exceed the price of that capital.

Infrastructure investing has all the time rewarded those that distinguish between building and worth creation. Airports, toll roads, and energy vegetation demand monumental funding lengthy earlier than they generate significant returns.

Throughout that interval, belongings develop, borrowings climb, fairness is raised, and money is consumed forward of earnings. Buyers who focus solely on present income typically miss the bigger story. What finally issues is whether or not administration earns returns that exceed the capital employed to construct these belongings.

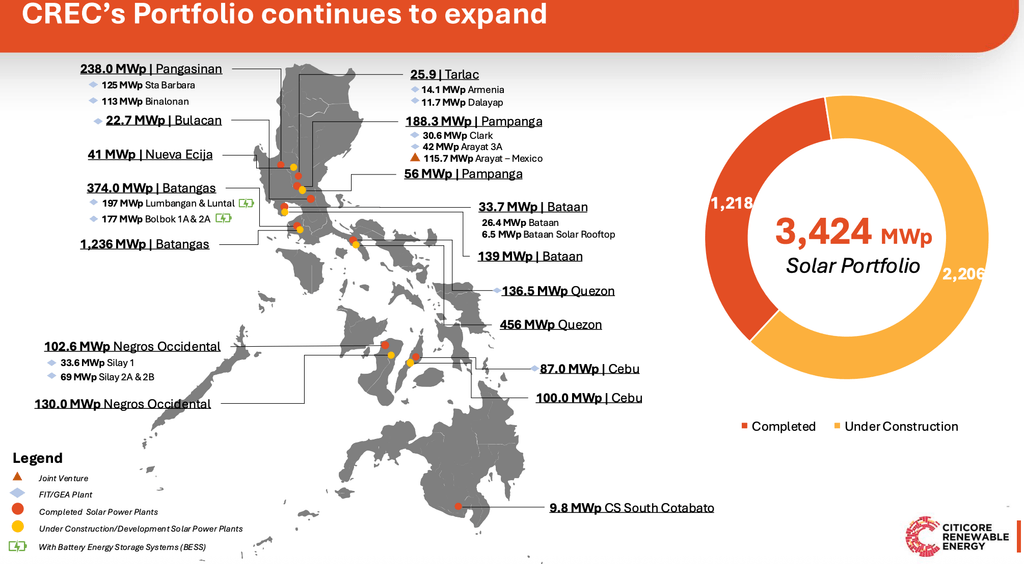

Citicore’s monetary profile displays an organization firmly in that funding part. Based mostly on its audited parent-company monetary statements, complete belongings elevated from P28.1 billion in 2024 to P40.6 billion in 2025, a 44% growth in a single yr. Fairness rose from P4.8 billion to P21.9 billion, supported by roughly P6.7 billion in contemporary capital, whereas complete borrowings climbed to roughly P14.6 billion. These figures painting an organization aggressively deploying assets somewhat than maximizing near-term profitability.

The financing sample is equally revealing. In the course of the yr, the father or mother generated solely about P125.5 million in working money whereas deploying greater than P10 billion into investments in subsidiaries, property additions, and advances throughout the company group. Internally generated money subsequently financed solely a small fraction of the growth program, with the stability coming from lenders and shareholders. That’s hardly uncommon in infrastructure. What is important to think about is whether or not right now’s investments finally generate returns that justify the capital dedicated.

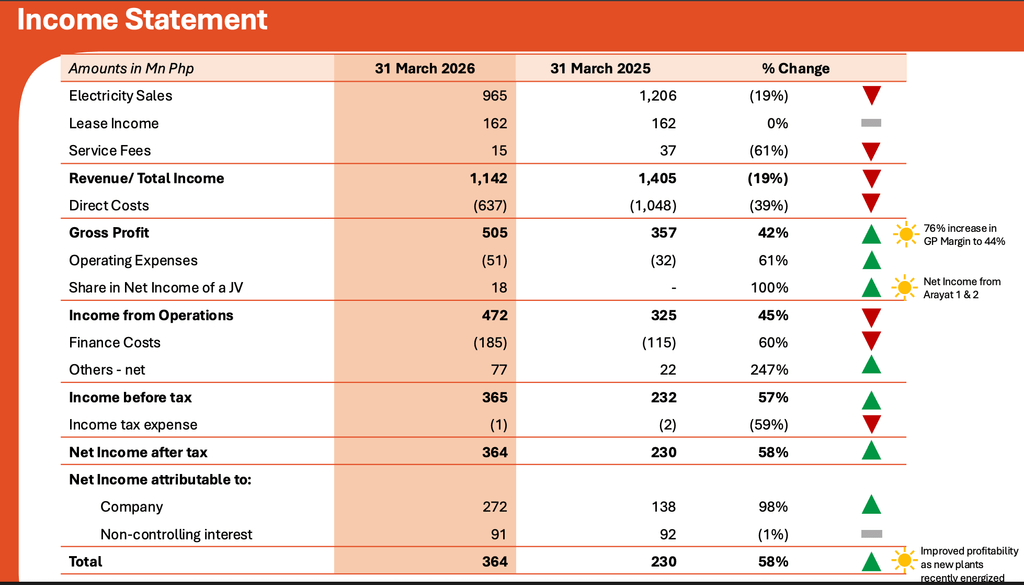

There are already indicators the technique is starting to work. Within the first quarter of 2026, CREC elevated web earnings 58% to P364 million whereas EBITDA rose 53% to P593 million, pushed largely by electrical energy gross sales from an increasing portfolio of working belongings. These outcomes counsel that investments made through the firm’s build-out part are starting to translate into working profitability.

One sturdy quarter, nevertheless, doesn’t eradicate execution danger. The actual take a look at is whether or not these earnings evolve into sturdy working money flows that may finance future growth with progressively much less reliance on exterior capital.

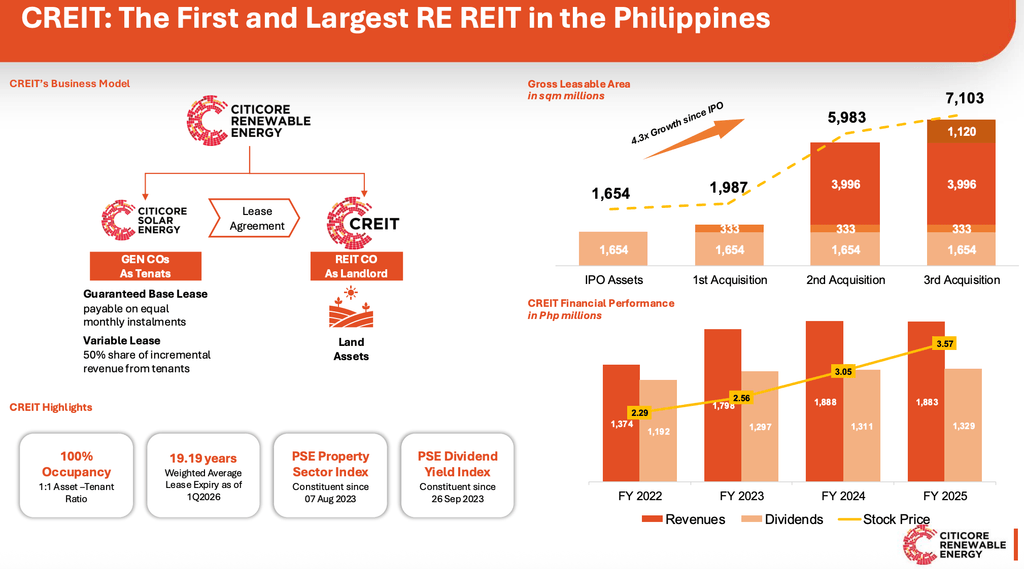

Understanding Citicore additionally requires understanding CREIT (Citicore Vitality REIT Corp.), the nation’s first renewable vitality actual property funding belief. Though each belong to the identical ecosystem, they carry out very completely different capabilities. CREIT owns renewable-energy actual property and earns recurring lease earnings from long-term contracts, offering secure money flows and dividends. Citicore Renewable Vitality develops, funds, constructs, and operates renewable-energy tasks. One owns mature belongings. The opposite creates them.

That relationship might grow to be Citicore’s best strategic benefit. Reasonably than completely retaining each accomplished asset, mature renewable properties can finally be monetized by means of CREIT, permitting capital to be recycled into the following technology of tasks.

International infrastructure traders, resembling Brookfield Asset Administration, Macquarie Group, and Blackstone Inc., have lengthy relied on comparable fashions to maintain progress whereas decreasing dependence on continuous debt and fairness elevating. If executed effectively, CREIT turns into greater than a landlord. It turns into one other supply of capital for growth.

Considered by means of that lens, Citicore shouldn’t be merely setting up photo voltaic farms. It’s assembling an built-in infrastructure platform wherein growth, operations, and actual property possession reinforce each other. The technique is financially logical. Whether or not it turns into financially rewarding relies upon nearly totally on execution.

That continues to be the principal funding danger. Infrastructure historical past is crammed with corporations that constructed spectacular asset portfolios however did not create shareholder worth as a result of tasks exceeded budgets, financing prices rose, or capital was allotted inefficiently. Renewable vitality is not any exception. Each peso borrowed should earn greater than its financing value, whereas each peso entrusted by shareholders should create worth past merely enlarging the stability sheet.

One merchandise deserves continued monitoring. Advances to associated events totaled about P5.8 billion, representing a significant portion of complete belongings. Such balances are widespread amongst infrastructure teams working by means of a number of subsidiaries and mission corporations, and they don’t by themselves counsel governance issues. They do, nevertheless, spotlight the significance of understanding how capital circulates throughout the broader Citicore ecosystem and whether or not these allocations persistently enhance long-term returns.

Buyers ought to likewise keep away from studying an excessive amount of into the father or mother firm’s year-on-year earnings decline. The comparability was closely affected by unusually giant one-off features and dividend earnings acknowledged in 2024. The extra significant measure shouldn’t be accounting revenue however whether or not right now’s investments mature into sturdy working money flows.

That’s the reason I imagine the query to be requested shouldn’t be whether or not GSIS made the appropriate funding. It’s far too early to reply that. The higher query is whether or not Citicore’s administration can persistently deploy billions of pesos into tasks that earn returns above their value of capital whereas utilizing CREIT’s capital-recycling platform to finance the following wave of progress.

If administration succeeds, GSIS will personal greater than shares in one other renewable-energy firm. It’s going to personal a stake in a classy infrastructure platform able to compounding worth for many years. If administration falls brief, fast balance-sheet growth will grow to be little greater than an costly accumulation of belongings with out commensurate shareholder returns.

Years from now, this funding is not going to be judged by the variety of photo voltaic panels put in or the gigawatts linked to the grid. It is going to be judged by a far easier measure: whether or not the billions of pesos deployed right now produce sturdy money flows and superior returns tomorrow. That’s the wager GSIS has made. – Rappler.com

Under are Vantage Level articles you will have missed:

Click on right here for different Vantage Level articles.